Legal & Tax Framework of Share-for-Share Transactions in M&A

Published on 2nd April 2025

Navigating the complexities of mergers and acquisitions requires a keen understanding of various transaction structures. Among these, share-for-share transactions stand out for their ability to align the interests of the parties involved and preserve cash reserves. This insight delves into the mechanics of share-for-share transactions, offering practical advice and highlighting key German legal and tax considerations.

1. Overview and Benefits of Share-for-Share Transactions

A share-for-share transaction involves the exchange of shares in one company for shares in another company. This type of transaction is typically used in mergers, acquisitions, or corporate restructuring where the acquiring company offers its own shares as consideration for the shares of the target company. Consequently, the shareholders of the target company receive shares in the acquiring company, rather than cash. Share-for-share elements are also frequently used in private equity transactions, where sellers and/or target company’s management often reinvest into the combined company structure. Another scenario is in the venture capital context, when a venture capital-backed company acquires competitors to conserve cash and tie sellers to the acquiring company. Angel investors and venture capital investors are usually paid in cash, while the founders sell part of their stake for cash and contribute the remaining part to a holding structure controlled by the acquirer, receiving shares in the holding entity. In these situations, the transaction is either completely structured as share-for-share or partially combined with a cash component.

2. Structure of a Share-for-Share Transaction

A share-for-share transaction is more complex to structure than a simple acquisition of shares with cash consideration. The scope of the share-for-share element, other elements of the purchase price, exchange ratio and valuation, the participation of all sellers in the share-for-share component, and the structure of the implementation should be discussed early on. A particular challenge can be the transfer of employees from one employee participation model to another at the level of the acquiring company.

From a tax perspective, the challenge with share-for-share transactions is that the transaction generally triggers a taxable capital gain, but the sellers do not receive any cash. To avoid this “dry income,” the German Reorganisation Tax Act (Umwandlungssteuergesetz – UmwStG) provides for a tax-neutral execution of share-for-share transactions under certain conditions.

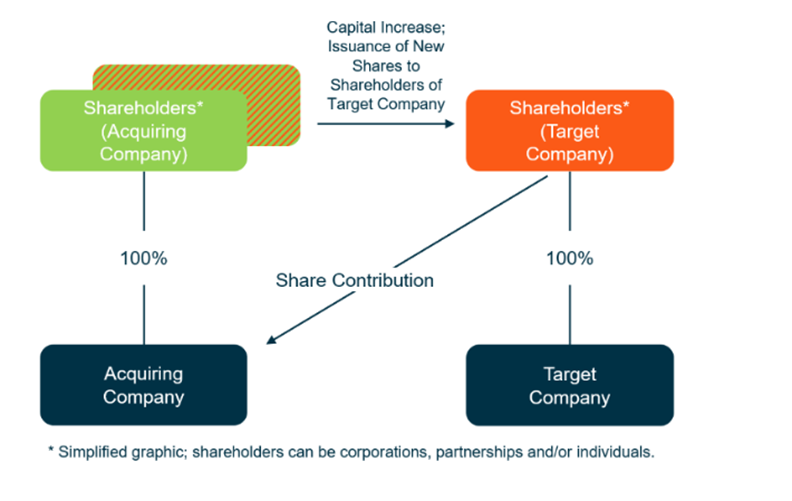

Under German corporate law, such participation can be realised either by contribution of the shares to the acquiring company in return for the issuance of new shares or via sale of the shares to the acquiring company in return for a cash payment followed by a reinvestment in the acquiring company. Most transactions with share-for-share elements are executed via the contribution approach to achieve tax-neutrality for the sellers.

3. Legal Challenges regarding the Technical Implementation of the Share-for-Share Component

The need for shares as "purchase currency" is a typical feature of share-for-share transactions. Usually, a capital increase is carried out at the level of the acquiring company. Even if sufficient treasury shares are available, a capital increase may become necessary as a tax-neutral share-for-share transaction requires the issuance of new shares in the acquiring company to the sellers.

One major challenge is structuring the process to allow timely implementation of the capital increase while safeguarding the interests of sellers and buyer. Timing and close coordination of the share-for-share component with the remainder of the transaction are particularly important.

From the sellers’ perspective, the contribution of shares in the target company should only take place if the sellers also receive the new shares in the acquiring company in return. As far as legally permissible, the contribution is therefore usually subject to the condition precedent of the registration of the capital increase at the level of the acquiring company in the commercial register. From the perspective of the acquiring company, it is imperative that the sellers, as holders of the new shares, also become subject to its contractual provisions. Consequently, the acquiring company will demand that the sellers accede to any existing shareholders' agreement upon closing with the subscription of the shares and be treated like any other shareholder within the corresponding share class.

3.1 Involvement of the Shareholders of the Acquiring Company

With respect to the necessary capital measures, the acquiring company and the sellers must deal with how to handle the rights of the shareholders of the acquiring company. In the case of a public limited company, the subscription rights of shareholders arise from section 186 of the German Stock Corporation Act (Aktiengesetz – AktG); the prevailing legal opinion applies the provision to the German limited liability company (GmbH) accordingly. The exclusion of statutory subscription rights requires a legitimate, objective business reason in the interests of the company and must be measured against the principle of proportionality. The most straightforward solution is often for the shareholders of the acquiring company to hold a shareholders' meeting upon completion, resolve upon the capital increase, and waive the exercise of their subscription rights. From the sellers’ point of view, this option is usually only viable if all or at least a quorum of the acquiring company's shareholders required for the capital increase resolution agree to participate in the capital increase vis-à-vis the sellers in the share purchase agreement. In practice, authorised capital is often used to enable the management to issue the required shares on completion of the transaction.

3.2 German Law Requirements for Raising and Maintaining Capital

In the context of the capital increase, the German capital raising regulations must be observed, which often leads to uncertainties in practice. A genuine capital increase with contribution in kind (Sachkapitalerhöhung) may be straightforward in legal terms but is unpopular from a practical point of view, as all the formal requirements for non-cash capital increases, including valuation and audit must be observed. A frequently used variant is the cash capital increase, in which the sellers subscribe to the new shares at nominal value and assign the shares to be sold to the company as "other additional payment" in accordance with section 272 (2) No. 1 or No. 4 German Commercial Code (Handelsgesetzbuch – HGB), usually referring to section 272 (2) No. 1 HGB, preferred from a tax perspective. This method, known as a cash capital increase with a premium in kind (Barkapitalerhöhung mit Sachagio), avoids the need to prove the value of the shares to be contributed to the commercial register if the value of the premium in kind is not negative and affects the lowest issue price of the shares.

However, this option may be problematic if the sellers receive additional cash compensation for the shares sold. In that case, there is a risk of the cash payment being considered a repayment of the shareholders’ contributions and a risk of a hidden contribution in kind (verdeckte Sacheinlage), leading to legal and personal risks for the managing directors of the acquiring company. This may not be a viable option for share-for-share transactions involving a public limited company as acquiring company.

Various alternative structures are proposed to avoid the risk of a hidden contribution in kind. We recommend a combination of a contribution in kind and an arms’ length transaction of a separable part of the shares in the target company: a portion of the shares transferred is determined as a contribution in kind and contributed to the acquiring company and another part of the shares transferred is sold in cash.

3.3 Acquiring Company is a German Public Limited Company (AG/SE)

If the acquiring company is a German or European public limited company (Societas Europaea), the legal room for manoeuvre is much more limited. Strict formal requirements for the involvement of shareholders, little leeway for the granting of guarantees, and stricter requirements for the raising and maintaining of capital further increase the complexity of share-for-share transactions when a public limited company is involved. This is all the more true if the shares of the acquiring company are listed on the stock exchange. Not only do the usual insider trading rules for transactions possibly apply, but the issuance of new shares must be incorporated into the capital market planning of the acquiring company. Prospectus obligations, black-out periods, admission of the new shares to trading, entry into the securities accounts of all sellers, and the negotiation and technical implementation of lock-up provisions to control the process of on-selling must then be considered.

In the best-case scenario, the public limited company as acquiring company has authorised capital, allowing the exclusion of subscription rights when carrying out transactions and not requiring the further involvement of the general shareholders’ meeting. This gives the board more flexibility in carrying out share-for-share transactions. If there is no authorised capital, a general meeting must be held to create new shares. It should also be borne in mind that the acquiring company may not provide financial assistance for the acquisition of shares. The granting of an advance payment or the provision of security for the acquisition of shares may be considered financial assistance, leading to the nullity of all concluded legal transactions.

4. Tax Aspects of Share-for-Share Transactions

Under tax law, share-for-share transactions involving shares in a corporation are referred to as "share swap". From a tax perspective, a share swap is similar to an exchange (tauschähnlicher Vorgang): The sellers exchange shares in the target company for new shares in the acquiring company. This results in the disclosure and taxation of hidden reserves available in the contributed shares, with the capital gain being the difference between the fair market value of the new shares and the book value of the contributed shares. This tax burden is dry income as the sellers do not receive any cash.

However, under certain conditions, the tax burden can be avoided, and the share swap can be executed neutrally, meaning hidden reserves available in the contributed shares are not disclosed but continued by the acquiring company. The relevant tax regulation for share swaps is section 21 of the German Reorganisation Tax Act. This tax privilege can be retroactively cancelled if the acquiring company does not maintain the status achieved by the share swap for a period of seven years.

4.1 Conditions for Application of German Reorganisation Tax Act

The German Reorganisation Tax Act covers contributions of both domestic and foreign shares in a corporation. However, restrictions apply with respect to the acquiring company, which must have its registered office and place of management in the European Union (EU) or the European Economic Area (EEA). In case of non-EU/EEA acquiring companies, a share swap always leads to a disclosure and taxation of hidden reserves available in the contributed shares. Individual sellers should negotiate a cash component to cover the resulting taxes.

The acquiring company must issue new shares to the sellers as consideration for the contribution of the shares in the target company. There is no minimum amount required for these new shares, and a small capital increase is theoretically sufficient. The actual amount often depends on various factors like valuation, number of sellers involved, and transaction background. If preference shares with specific characteristics are issued, a thorough tax analysis is recommended: In case such shares are economically comparable to a shareholder loan, they might be treated as “other assets” (sonstige Gegenleistung) and affect the tax-neutral status of the share swap.

4.2 Valuation of the Contributed Shares

At the Level of the Acquiring Company the contributed shares must generally be recognised at fair market value in the tax balance sheet. However, if the acquiring company holds the majority of voting rights in the target company after the contribution (a "qualified share swap"), it can apply to continue the book values / acquisition costs or recognise an intermediate value (Zwischenwert). This application must be submitted by the acquiring company to the tax office at the latest by the time the tax balance sheet for the financial year of the contribution is submitted for the first time. It can also be implied through respective recognition in the tax balance sheet but a written application in timely connection to the share swap is recommended. If, in addition to the new shares, the sellers receive other assets as consideration whose fair market value exceeds (i) EUR 500,000 or (ii) the book value of the contributed shares, the acquiring company must recognise at least the fair market value of the other assets, resulting in an intermediate value.

At the Level of the Contributing Shareholder the tax treatment of the share swap for sellers is generally linked to how the acquiring company recognises the contributed shares. The recognised value is deemed the selling price of the contributed shares and the acquisition cost of the new shares. If recognised at book value, the share swap is tax-neutral for the sellers; if recognised at fair market value, a taxable capital gain arises (if recognised at intermediate value, the share swap results in a partial tax neutrality for the sellers). Sellers should negotiate protection clauses requiring the acquiring company to apply for book value continuation if the conditions are met. In cross-border share swaps, the “value link” does not work as the recognition at the level of the acquiring company is based on foreign law. For a qualified share swap, if, after the contribution, the German taxation right with respect to a capital gain on the new shares is not excluded or limited, sellers can apply for a book value continuation or recognition of an intermediate value. This application must be submitted to the tax office by the time the tax return for the assessment period of the contribution is submitted for the first time. A further exception to the “value link” applies to individual sellers holding less than 1% of the shares in the target company’s shares for private purposes (Kleinanleger). Section 20 para 4a of the German Income Tax Act (Einkommensteuergesetz – EStG) as special regulation preceding the German Reorganisation Tax Act stipulates that, under certain conditions, the acquisition costs must be carried forward making the contribution tax-neutral.

4.3 Further Tax Consequences for Individual Sellers

If an individual seller executes a share swap below fair market value according to the German Reorganisation Tax Act, the contributed shares are subject to a seven-year lock-up period. If sold during this period or if a "detrimental event" occurs, the share swap’s tax-neutrality is retroactively denied, and hidden reserves available in the contributed shares at the time of the contribution are disclosed and taxed (contribution gain). The contribution gain is reduced by one-seventh for each full year passed since the contribution. The lock-up period ends after seven years from the date of contribution or earlier if the new shares in the acquiring company are sold or subject to exit taxation under the German Foreign Tax Act (Außensteuergesetz – AStG). In addition, annual evidence must be provided to the tax office by May 31 at the latest during the lock-up period, showing who is the (beneficial) owner of the contributed shares at the relevant anniversary date of the contribution. Failure to provide this evidence results in a deemed sale of the contributed shares, resulting in a contribution gain for the individual seller.

Any breach of the lock-up period is triggered by the acquiring company, but with tax consequences for individual sellers, given that a contribution gain is dry income. After the share swap, the sellers often lose influence over the contributed shares. Therefore, sellers should ensure that the legal documentation includes precautionary measures. Similarly, the annual evidence information does not relate to the sellers personally, but rather to the acquiring company. Cooperation clauses obliging the acquiring company to assist are recommended.

5. Conclusion

The strategic use of share-for-share transactions can significantly benefit companies looking to grow and align stakeholder interests. These transactions, while complex, offer the advantage of preserving cash and potentially achieving tax neutrality. Companies must approach these transactions with a comprehensive understanding of the legal and tax frameworks involved. By leveraging expert advice and careful planning, businesses can maximise the benefits and mitigate the risks associated with share-for-share transactions.

You can find an extended version of this insight in the M&A Review.